There is no single "economy" to plan around anymore. There are two, diverging — and which one your customers live in matters more than any headline GDP number.

Two CEOs sit at the same conference, in the same week, looking at the same GDP print. One says the economy has never felt stronger — orders are up, valuations are rich, capital is cheap to him. The other says his customers are tapped out, trading down, cancelling. Both are telling the truth. Neither is describing the average.

That is the strange feature of the moment. The headline number — growth, the aggregate, the single figure that leads the newsletter — has stopped describing a world that anyone actually lives in. It describes a midpoint between two economies that are pulling apart, and almost no real customer sits at that midpoint.

The single economy is dead

For most of the postwar period, a national economic number meant something operational. When GDP rose, broadly, most people and most businesses felt it. The average was a decent proxy for the typical experience. You could plan to the aggregate and not be badly wrong.

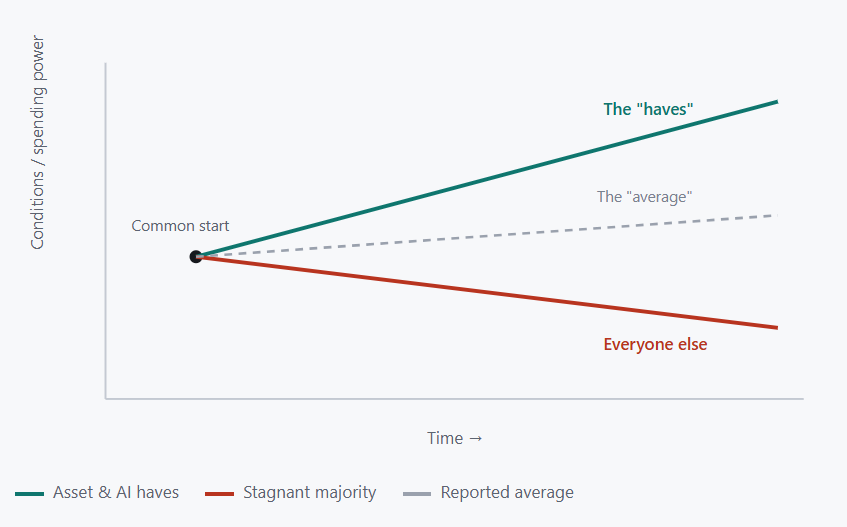

That link has frayed. What we have now is closer to a K: a common starting point from which two trajectories diverge. One arm rises — the holders of assets, the AI and capital "haves," the high-skill service and finance firms riding a wave of investment and pricing power. The other arm runs flat or bends down — large swaths of the consumer base and the businesses that serve them, where investment is thinner and gains are slow to arrive.

The average of those two arms is a line that points gently up and tells you almost nothing. It is the temperature of a patient with one foot in ice and one in boiling water.

Visual 1 — The shape of the divergence

Illustrative. The dashed line is the number you read in the headline. It sits between two trajectories and matches the lived reality of neither group. Planning to the dashed line means planning for a customer who doesn't exist.

What's driving the wedge

This is not a story of bad luck spread evenly. The split has an engine, and the engine is concentration.

Capital and gains are pooling in a narrow band of the economy — AI and a handful of favored sectors — while investment elsewhere runs weaker. The productivity and income gains that do show up are uneven by design: the forecasts that look out across 2026 expect them strongest in high-skill services and finance, precisely the corners already on the upper arm. The rising line rises because the money, the tools, and the pricing power keep concentrating where they already are. The flat line stays flat for the mirror-image reason.

For a business, the consequence is blunt. If your customers are concentrated on the upper arm, you are operating in a boom and should plan like it. If they sit on the lower arm, you are in something closer to a slow recession, whatever the headline says. The aggregate cannot tell you which — it has averaged the answer away.

The argument that isn't worth having

Most of the public debate about the economy is a fight between "it's fine" and "it's terrible," conducted by people who are each looking at one arm of the K and mistaking it for the whole letter.

"The economy is fine" and "the economy is terrible" are both true at once. Leaders arguing over which one is right are answering a question that no longer has a single answer — the useful question is which economy your customers live in.

That is the contrarian turn, and it is more than rhetorical. The bull and the bear are both correct, which means neither side's macro call gives you anything to act on. The strategic information isn't in the aggregate at all. It's in the distribution — in knowing precisely which arm your buyers are riding, because that single fact will shape your pricing, your positioning, and your forecast more than any number on the news.

Visual 2 — The two economies, side by side

| The upper arm | The lower arm |

|---|---|---|

Who's here | Asset holders, AI/capital winners, high-skill services & finance | Wage-dependent consumers, thin-margin SMBs, their suppliers |

Conditions | Booming — cheap capital, pricing power, rising gains | Stagnant — squeezed budgets, weak investment, trading down |

What they buy | Premium, capability, speed; price is secondary | Value, durability, essentials; price is the decision |

How to serve them | Sell outcomes and edge; protect premium positioning | Sell certainty and value; protect access and affordability |

How to use it: sort your real customer base into these two columns. A book split across both is two businesses wearing one logo — and usually needs two strategies.

Strategy is now a segmentation problem

Once you accept the K, a lot of conventional planning starts to look like a category error. A single price point aimed at "the market" will be too high for one arm and leave money on the table with the other. A single message that works in a boom lands as tone-deaf in a downturn, and the two arms are living in both at the same time.

The companies that navigate this well stop asking "how is the economy doing?" and start asking "how is my economy doing?" They build the divergence into the model: separate value propositions for separate arms, pricing that reflects which reality a segment occupies, and a refusal to be whipsawed by aggregate data that describes neither. The ones that struggle are the ones still managing to the average — setting one strategy for a midpoint customer who turns out to be a statistical ghost.

What this means for leaders

Stop forecasting from the headline number. The aggregate has become a poor proxy for what your buyers actually feel. Build your demand model from the bottom up — by segment, by which arm of the K each segment rides — and treat the national figure as background, not signal.

Find out which economy you sell into, exactly. Most companies have never explicitly mapped their customer base onto the divergence. Do it. If you're concentrated on the upper arm, you can lean into premium and capability. If you're on the lower arm, durability and value are not a fallback — they're the whole game.

Price and position for divergence, not for the middle. A single offer aimed at the average will misfire on both arms at once. Where your customers span the K, accept that you may be running two strategies under one roof — and resource them as two, rather than splitting the difference and serving no one well.

There is no single economy to plan around, and pretending otherwise is the most common strategic mistake of the year. The headline is an average of two worlds. Your customers live in one of them. Knowing which is no longer market research — it's the strategy.

Context drawn from: Deloitte, "United States Economic Forecast" (Q1 2026), EY, "CEO Outlook" (2026), and reporting on uneven, AI-driven investment concentration.