For thirty years, the smartest move was to source from wherever was cheapest and hold as little inventory as possible. That era is over, and the replacement costs more on purpose.

There's a particular kind of executive who came up in supply chain over the last three decades, and you can spot them by their reflexes. Show them a sourcing decision and they reach instinctively for the lowest landed cost. Show them a warehouse and they want to know why it's full. Inventory was waste. Distance was fine as long as the unit price was right. The whole discipline organized itself around a single verb: trim.

Those reflexes were correct for a long time. They are now actively dangerous, and the people running supply chains know it.

The old optimum was elegant in its simplicity. Find the cheapest competent source on the planet, regardless of where it sat. Hold the minimum inventory the system could tolerate — just-in-time, lean, nothing sitting idle. Every link tuned for cost, every buffer shaved, every mile justified by arbitrage. For three decades of stable trade and quiet geopolitics, this produced the lowest cost per unit anyone had ever seen, and it rewarded the firms most ruthless about pursuing it.

The reflex survives. The conditions that justified it do not.

The risk got repriced

What changed isn't fundamentally about any one tariff schedule, and treating it that way is the mistake the laggards are making. A tariff is a symptom. The underlying shift is that the geopolitical risk embedded in a long, concentrated, single-source supply chain — risk that sat unpriced for thirty years because nothing came due — is now being priced. A pandemic priced it once. A blocked canal priced it again. Trade restrictions and the threat of more keep pricing it. The market has learned that the cheap chain carried a tail risk it never paid for, and it's now charging for that risk in real time.

The numbers describe a redirection, not a tweak. Roughly 77% of supply-chain leaders have shifted sourcing away from China toward tariff-neutral countries. About 87% are increasing buffer inventory — the very thing the old religion called waste. Another 87% plan to run nearshoring pilots in Mexico or Central America within twenty-four months. And about 75% of retail supply-chain leaders say tariff turbulence is actively redefining their 2026 strategy. When three-quarters of an industry moves in the same direction inside a single planning cycle, that's not a hedge. That's a reset.

From efficiency to resilience

The consensus framing has settled on a sentence: efficiency takes a back seat to resilience. It sounds soft until you sit with what it actually means. It means a generation of optimization logic — the math that said shave the buffer, lengthen the supply line, concentrate the source — has been demoted from first principle to one consideration among several. The objective function changed. You no longer minimize cost subject to keeping the lights on. You maximize the odds of keeping the lights on, subject to a cost you're now willing to bear.

This is the part worth stating sharply, because it cuts against thirty years of received wisdom about what "efficient" even meant.

The lean, just-in-time, lowest-cost supply chain was never efficient in any honest sense. It was cheap because it refused to price its own risk. Now the risk has a price, and companies are paying more for control because control turned out to be the thing they were actually buying.

Read that contrarian turn carefully, because it reframes the whole conversation. The companies adding cost right now are not abandoning efficiency. They are correcting a thirty-year mispricing. A system that produces the lowest unit cost while quietly accumulating catastrophic tail risk is not an efficient system; it's a leveraged bet that nothing goes wrong, dressed up as operational excellence. Paying for resilience isn't waste creeping back in. It's the bill for risk that was always there and is finally being settled.

Visual 1 — Efficiency era vs. resilience era

Dimension | Efficiency era (1995–2020) | Resilience era (2020– ) |

|---|---|---|

Sourcing | Cheapest competent source, anywhere | Diversified, regional, tariff-aware |

Inventory | Minimal; just-in-time; buffers are waste | Buffer stock as deliberate insurance |

Priority | Lowest landed cost per unit | Continuity and control of supply |

Optimizes for | Cost in a stable world | Survival in an unstable one |

What it costs | Hidden tail risk, unpriced | Higher unit cost, paid on purpose |

How to read it: the right column isn't a downgrade from the left. It's the same trade-off with the risk finally added back into the price.

Why companies pay willingly

The striking thing about this shift is that nobody's being forced into it kicking and screaming. Firms are choosing higher cost with their eyes open, because they've run the other experiment and seen the bill. A factory idled for want of one component sourced from one place teaches a lesson that no spreadsheet ever did. A shelf empty during peak demand costs more than years of buffer inventory would have. Once you've paid the price of fragility once, paying a steady premium for resilience stops looking like waste and starts looking like the obvious trade.

And the persistence is the whole point. Strip away every current tariff tomorrow and the strategic logic survives intact, because the logic was never really about tariffs. It's about not wanting a single political decision in a single capital to be able to halt your business. That exposure exists regardless of which duties are in force this quarter. The reset is multi-year and structural precisely because the thing driving it — concentrated geopolitical risk — doesn't disappear when one policy does.

The regionalization map

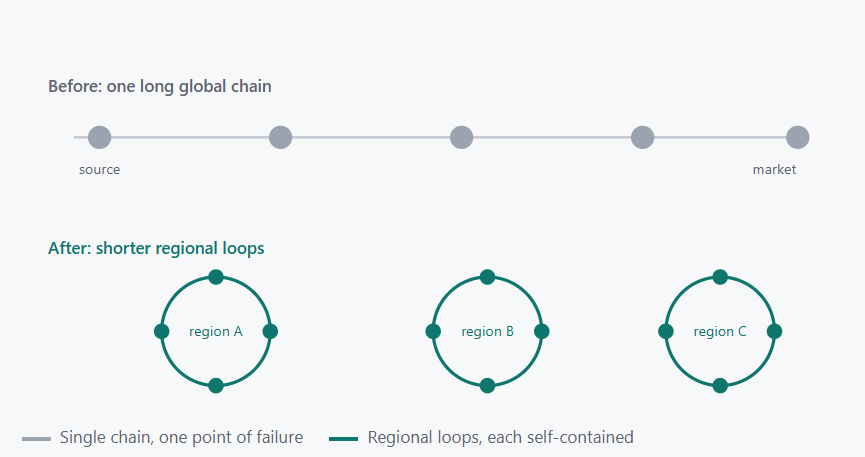

What's emerging isn't a return to making everything at home. It's regional. The long single chain spanning the planet is fracturing into shorter loops that stay closer to demand: nearshoring into Mexico and Central America for North American markets, supplier diversification so no single country holds the off switch, buffer inventory positioned to absorb the shock when one node stumbles. Reshoring is a piece of it, but the real shape is regionalization — production organized around continents rather than around the single cheapest dot on a world map.

Visual 2 — From one long chain to regional loops

Illustrative. The shift in one picture: stop running one fragile line across the planet, start running several shorter loops that each survive on their own.

Winners and the new trade-off

The winners are the firms that move while it's still a choice rather than a scramble. Companies that built supplier diversity before they needed it, that positioned regional capacity ahead of the rush, that learned to carry buffer without letting it metastasize into dead stock — they get resilience at a manageable premium. The losers will be those who clung to the lowest-cost chain one disruption too long, then had to rebuild under duress, paying peak prices for nearshore capacity that everyone else is bidding for at the same time.

The new trade-off is honest in a way the old one wasn't. You will pay more per unit, and you will know exactly what you're buying with the difference: the ability to keep operating when something breaks. The era of pretending that cost and risk were the same number is over. The companies that price both, deliberately, are the ones that will still be shipping when the next shock arrives.

What this means for leaders

Stop treating resilience spend as waste to be justified. The buffer inventory and the second supplier aren't inefficiencies that crept back in. They're the premium on an insurance policy you were running without for thirty years. Budget them as insurance, evaluate them as insurance, and stop asking the supply-chain team to apologize for them.

Separate the tariff noise from the structural signal. Specific duties will rise and fall with politics. The reason to diversify and regionalize won't, because it rests on geopolitical concentration risk that outlasts any single policy. Build for the structural reality, not the headline, and you won't have to re-decide this every time the trade news shifts.

Move before the rush prices you out. Nearshore capacity, regional suppliers, and the talent to manage them are finite, and everyone is reaching for them at once. The firms securing relationships now will hold them at reasonable terms. The ones waiting for certainty will pay scarcity prices for the same resilience, later, under pressure.

The frictionless supply chain was a product of an unusually calm thirty years. That calm is gone, and it isn't the kind of thing that comes back on schedule. The chains being built now cost more by design — and the leaders building them understand they're not overpaying. They're finally paying the real price.

Sources: FreightWaves, "Tariff volatility pushes global supply chains into regional reset in 2026"; Inbound Logistics, "Beyond Reshoring to Regionalization"; and BOK Financial, "Is the U.S. Leading the Dance of Deglobalization?"