A handful of companies are spending more on AI infrastructure this year than most countries spend on anything. The whole economy is now leaning on that wager paying off.

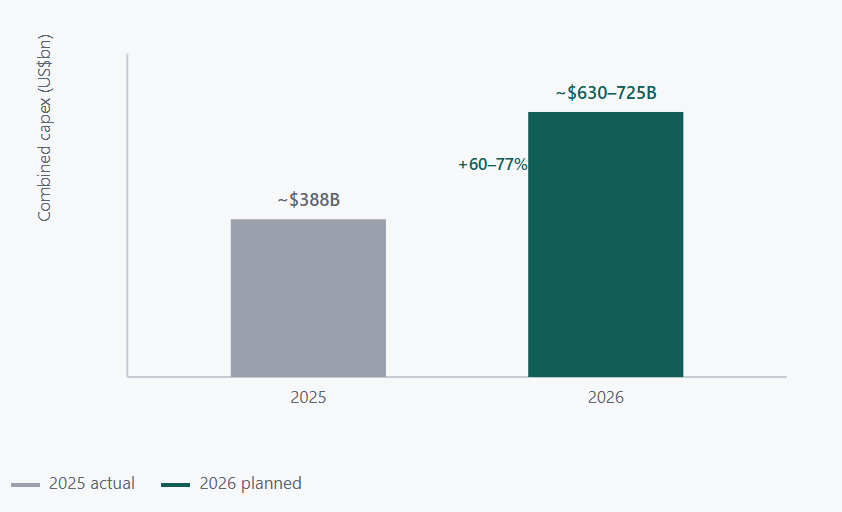

Picture the capital budgets of four companies laid end to end. This year, those four plan to spend somewhere between $630 billion and $725 billion building AI infrastructure — chips, data centers, the power to run them. That is more than the annual government budget of most nations on earth, committed by four boards, on the conviction that machine intelligence is the next utility.

Roughly three-quarters of that — call it $450 billion — is AI-specific. Amazon is putting up around $200 billion. Google, $175 to $185 billion. Meta, $115 to $135 billion. Microsoft, $110 to $120 billion. A year ago the same group spent about $388 billion all in; the jump to 2026 is on the order of 60 to 77%. There is no peacetime precedent for private capital moving at this scale and speed toward a single thesis.

Visual 1 — The step change

Illustrative. Combined planned capex of the four largest hyperscalers. Roughly three-quarters — about $450B — is AI-related. A jump of this size in a single year, from a base this large, is the part with no real precedent.

Why everyone is exposed, not just tech

It would be easy to file this as a tech-sector story — interesting if you hold the stocks, irrelevant otherwise. That would be a mistake, because the bet has become load-bearing for the broader economy in a way that reaches well past the companies writing the checks.

Capital spending on this scale shows up in the national accounts. It is propping up construction, electrical equipment, power generation, and the contractors and suppliers feeding all three. It is a meaningful share of the market's gains, concentrated in a handful of names that now anchor index funds and pension portfolios. When a few firms account for so much of the spending and so much of the valuation, their wager stops being theirs alone. The economy has co-signed it.

That is the uncomfortable truth beneath the optimism. The AI buildout is no longer a sideshow to growth. In important respects, it is the growth.

The bull case and the bear case

The bull case is straightforward and, on its own terms, credible. Demand for compute genuinely outstrips supply; operators say, repeatedly and with money behind the words, that they cannot build capacity fast enough. If AI becomes the substrate of knowledge work, today's spend is the foundation of the next productivity era, and underbuilding would be the real error.

The bear case is just as coherent. Most enterprises are not yet seeing measurable returns from AI — one survey found 56% reported neither revenue gains nor cost cuts from it. Much of the spending is circular, hyperscalers buying from chipmakers they're invested in, customers funded by the vendors they buy from. The infrastructure depreciates fast. And revenue has so far lagged the capital pouring into the ground by a wide margin.

Visual 2 — The two sides of the wager

Dimension | Bull case | Bear case |

|---|---|---|

Demand | Operators can't build fast enough; capacity is the constraint | Demand is real but won't justify spend at this price and pace |

Returns | The productivity payoff is coming; early ROI always lags | 56% of firms see neither revenue gains nor cost cuts yet |

Structure | Vertical integration secures supply for the long build | Circular financing inflates apparent demand |

Risk if wrong | Underbuilding cedes the next platform to rivals | An overbuild unwinds and bruises the whole market |

How to read it: both columns can be partly right. The bull and bear aren't really arguing about whether AI matters — they're arguing about price, pace, and timing of the return.

Right about the technology, wrong about the return

Here is the turn that most of the debate misses, because the debate is stuck on the wrong question. People argue about whether AI is real, as if that settles whether the capex is wise. It doesn't.

Being right about the technology and wrong about the returns are entirely compatible. The internet was transformative and still vaporized a trillion dollars of capital on the way to proving it. The technology can be everything its champions claim and the investment can still be a bad one at this price.

The railroads were real and reshaped the continent — and most of the companies that laid the track went bankrupt, their overbuilt lines bought for cents by the survivors. Fiber in the late 1990s was real and underpins everything you do online today — and the firms that buried it largely cratered first. Transformative technology and ruinous investment are old companions. The gap between "this changes everything" and "this was a good place to put the money at that valuation" is exactly where the risk in the AI bet lives. It is not a question about silicon. It is a question about price and pace.

What a wrong bet would mean beyond tech

If the returns arrive on schedule, the buildout becomes the most consequential capital deployment of the era and the bears look timid. If they lag badly, the unwind would not stay contained. Spending tied to AI construction would slow, taking the suppliers and contractors with it. The concentrated valuations would correct, and because those names sit in nearly every diversified portfolio, the pain would travel to people who never bought an AI stock on purpose. A bet this large, made by this few, simply cannot fail quietly.

What this means for leaders

Map your indirect exposure, even if you're not in tech. You may have more riding on this bet than you think — through your index holdings, your customers' health, the macro growth your plan assumes. Trace the lines. The buildout is holding up parts of the economy you depend on, whether or not you ever bought a GPU.

Separate the technology question from the investment question. Believing AI will reshape your business does not commit you to believing the current capex will pay off on the current timeline. Adopt the technology where it earns its keep; don't let conviction about the tech smuggle in conviction about the market's pricing of it.

Plan for both branches, because you can't pick. If the bet pays off, you want to be using AI in anger, not catching up. If it unwinds, you want a plan resilient to a market correction concentrated in the names everyone owns. The leaders who fare best won't be the ones who called it — they'll be the ones who didn't need to.

This is the largest concentrated wager private capital has made in a generation, and the whole economy is leaning on it. It may well be the foundation of the next era. It may also be the most expensive lesson in the difference between being right about a technology and right about its price. Both are still on the table.

Context drawn from: CNBC, "Big Tech's AI spend approaches $700 billion in 2026", Tom's Hardware, "Big Tech's AI spending plans reach $725 billion", and PwC, "2026 Global CEO Survey."