For decades, the state was supposed to stay out of the way and let markets allocate. That consensus is gone. Governments are picking sectors, subsidizing factories, and using tariffs as strategy — and business has to plan around it.

A factory breaks ground in Arizona that, on any honest spreadsheet, should have been built in Taiwan. The cost per wafer is higher. The talent pool is thinner. The supply chain is half-assembled. And it gets built anyway, because a government decided it should — and wrote a check large enough to bend the arithmetic.

That single image tells you most of what changed. For a generation, the working assumption inside corporate planning was that capital flowed to wherever the math was best, and the job of the state was to stay out of the way. Comparative advantage did the allocating. Governments set the rules and refereed.

That assumption is no longer safe to build a strategy on. The state has walked back onto the field — not as referee, but as a player with a checkbook and a thesis about which industries it intends to own.

What the new playbook actually looks like

Industrial policy is back, and it does not announce itself as a single grand program. It shows up as a toolkit, deployed sector by sector. Subsidies for chip fabs and battery plants. Tariffs that double as revenue and as a lever to pull factories home. Export controls on the most advanced semiconductors. Domestic-content rules that quietly rewrite where a thing must be made before it qualifies for support.

The tariff piece is the clearest tell. Tariffs are no longer treated mainly as a negotiating chip to be lifted once a trade deal is signed. They are being used as a standing instrument — a way to raise revenue and, more pointedly, to make domestic production the rational choice rather than the patriotic one. When the duty on an imported component is steep enough, "build it here" stops being a slogan and starts being the cheaper option.

The corporate response has already moved. Roughly 77% of supply-chain leaders report shifting sourcing away from China — not as a one-off hedge, but as a structural rebuild of where their inputs originate. That is not a rounding error in procurement. That is the map being redrawn.

Visual 1 — Two operating assumptions

Question | Neutral-market assumption | Industrial-policy reality |

|---|---|---|

Where is value made? | Wherever cost and skill are lowest | Where policy steers it — favored sectors, favored borders |

Who decides the winners? | The market, through prices | The market and the state, through subsidies and rules |

What are tariffs? | A temporary friction to wait out | A standing revenue and investment tool |

What do subsidies signal? | Distortion to be ignored | A durable thumb on the scale to plan around |

How do you site a plant? | Optimize landed cost | Optimize landed cost after incentives and content rules |

How to read it: the left column is the world most corporate strategies were built for. The right column is the one those strategies now have to survive in.

Structural, not a phase

It is tempting to file all of this under "current administration, current cycle" and assume the pendulum swings back. That reading is comfortable and probably wrong.

The forces underneath are not partisan and not temporary. Supply-chain fragility was exposed in a way that boards will not forget. Security concerns over chips, energy, and critical minerals cut across the political spectrum. And the largest capital event of the decade — the buildout of AI and the energy to power it — is itself being steered by policy, because no government wants to depend on a rival for the compute and electricity its economy will run on. When the strategic logic and the political logic point the same direction, you are not looking at a phase. You are looking at the new default.

Capital has read the signal already. Investment is concentrating, visibly, in the sectors governments have blessed — AI infrastructure and domestic manufacturing above all. Money flows toward where the subsidies, the contracts, and the protection are. That is not a distortion waiting to correct. That is the system working as designed.

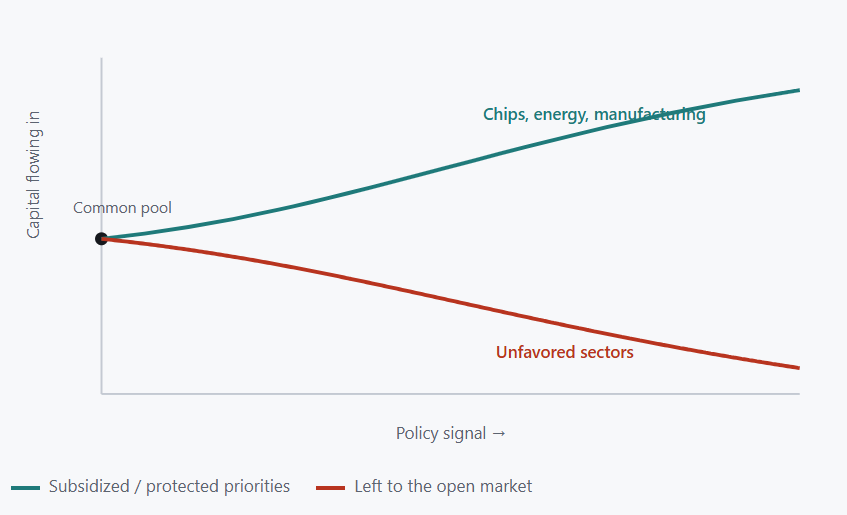

Visual 2 — Capital bends toward the favored

Illustrative. From a common pool of investable capital, policy bends the flow. The sectors a government chooses to back pull money toward them; the rest are left to compete for what remains.

Winners get manufactured too

Here is where most of the commentary goes lazy. The reflex is to treat industrial policy as unambiguously bad for business — friction, distortion, inefficiency, a tax on the productive imposed by the political.

That framing misses the move. A government writing checks and raising walls does not destroy value so much as relocate it. For every company stranded on the wrong side of a content rule, there is one whose plant just became the only compliant supplier in the market. For every importer crushed by a tariff, there is a domestic producer handed a moat it could never have built on its own.

Industrial policy doesn't abolish winners. It chooses them in advance — and the most expensive mistake a leader can make is to treat that choice as noise to be waited out rather than a market force to be played.

The companies that will look prescient in five years are not the ones that complained loudest about distortion. They are the ones who read the policy map early, sited their capacity where the incentives pointed, and qualified for the support before their competitors filed the paperwork. Alignment with the subsidized priority is now a real source of advantage — as real as a cost edge or a patent.

The trap of planning for a neutral world

The deepest risk is not any single tariff. It is a mental model. Plenty of strategies still assume, somewhere in their bones, that markets are neutral arbiters and that government action is temporary interference to be optimized around until it passes.

Build on that assumption and you will systematically misjudge where value pools. You will site for landed cost and miss the incentive stack. You will treat a content rule as red tape rather than a market-access gate. You will wait out a tariff that is not going anywhere. None of these are dramatic errors on any given day. Compounded over a capital cycle, they are the difference between owning the new map and being stranded on the old one.

What this means for leaders

Treat policy as a market force, not a weather event. You model interest rates, demand, and competition. Put government direction in the same tier of your planning. The question is no longer "will this intervention pass?" but "which sectors and borders is the state committed to, and how do we sit on the right side of that line?"

Read the incentive stack before you read the cost sheet. Landed cost is now the answer to a question that comes second. Site selection, sourcing, and product design should run through subsidies, content rules, and tariff exposure first — because those can swing the economics more than any operational efficiency you'll find.

Decide deliberately whether to align or to hedge. Aligning with a favored sector buys you support and a moat, at the cost of dependence on a political choice that could shift. Staying neutral preserves flexibility and forfeits the subsidy. Either can be right. Drifting into one by inattention is the only clearly wrong move.

The hands-off consensus is not coming back on any timetable a company can plan around. The governments writing the checks have decided which industries they intend to own, and they are pricing the rest of us in or out accordingly. You don't have to like it. You do have to plan for it.

Context drawn from: BOK Financial, "Is the US Leading the Dance of Deglobalization?", FreightWaves, "Tariff volatility pushes global supply chains into a regional reset in 2026", and Brookings, "Global energy demands within the AI regulatory environment."