A business can be profitable on paper and insolvent in practice. The number that actually keeps the lights on is timing — when cash arrives versus when it leaves — and most leaders barely watch it.

The board meeting was a celebration. Revenue up 60 percent year over year, gross margin holding, a net profit on the slide that earned a round of nods. Three weeks later the same company couldn't make payroll without a bridge loan it took at a punishing rate. Nothing had gone wrong with the business. The business was the problem.

This is the failure mode nobody puts on the growth slide. A company can post a profit every quarter and still run out of money, because profit and cash are not the same thing and almost never arrive at the same time. Profit is an accounting position — an opinion about a period, full of accruals and recognition rules and revenue you've earned but haven't been paid. Cash is the balance in the account when the supplier invoice clears. One is a narrative. The other is a fact.

Most leaders manage the narrative. They read the P&L line by line and treat the cash flow statement as the accountant's department. That gets the priority exactly backwards. The P&L tells you whether the business model works. Cash tells you whether the business survives long enough to find out.

You pay before you get paid

The mechanism that quietly kills profitable companies has a dry name — the cash conversion cycle — and a simple meaning. It's the gap between the day money leaves your account and the day it comes back.

Walk the sequence. You buy raw materials or commit to a service delivery. Payroll runs every two weeks regardless of who has paid you. You ship the product or complete the work. You send an invoice. The customer, operating on their own terms and their own convenience, pays in 45 or 60 or 90 days. Between the cash going out and the cash coming back is a hole, and you are funding it the entire time. The bigger and faster the business, the more orders sit inside that hole at once.

A company with healthy margins and a 70-day cash gap is borrowing — from a bank, from a credit line, or from its own dwindling reserves — to finance its own customers. It is, in effect, a lender that also happens to make a product. Profit doesn't close that gap. Only collected cash does.

Visual 1 — Profit view vs. cash view

Same growing business | Profit view (the P&L tells you) | Cash view (the bank account tells you) |

|---|---|---|

Revenue, this quarter | $4.0M booked, up 60% YoY | $2.6M actually collected |

Net result | $340K profit — looks healthy | $210K cash burned — actually starving |

Receivables | An asset on the balance sheet | $1.4M sitting in customers' accounts, not yours |

Effect of growth | Bigger top line, bigger profit | Wider gap, faster burn |

The verdict | "Best quarter we've had." | "We need a bridge loan by the 30th." |

Conceptual model. Two readings of one company in the same period. The left column is what gets celebrated in the board deck. The right column is what determines whether the company is still here next quarter.

Growth widens the hole

Here is the part that breaks people's intuition, and it's the whole argument: growth is a cash consumer, not a cash generator.

The instinct says the opposite. More sales, more money, more cushion. But a profitable order with a 70-day cash gap doesn't hand you cash — it hands you a 70-day liability you have to fund before the payment arrives. Double your order volume and you double the amount of cash trapped in transit at any moment. The faster you grow, the more capital the growth itself swallows. A company can grow straight into insolvency while every individual deal is profitable, which is precisely why the death is so confusing from the inside. Nobody made a bad sale. They made too many good ones, too fast, on terms that funded the customer.

Profit is an opinion; cash is a fact. And fast, profitable growth on a broken cash cycle doesn't save you — it's the accelerant.

This is why hypergrowth companies raise money they don't appear to need. The outside read is "they're profitable, why dilute?" The inside read is that the working capital required to fund the next year of growth exceeds anything the business can throw off on its own. The raise isn't covering losses. It's covering the gap.

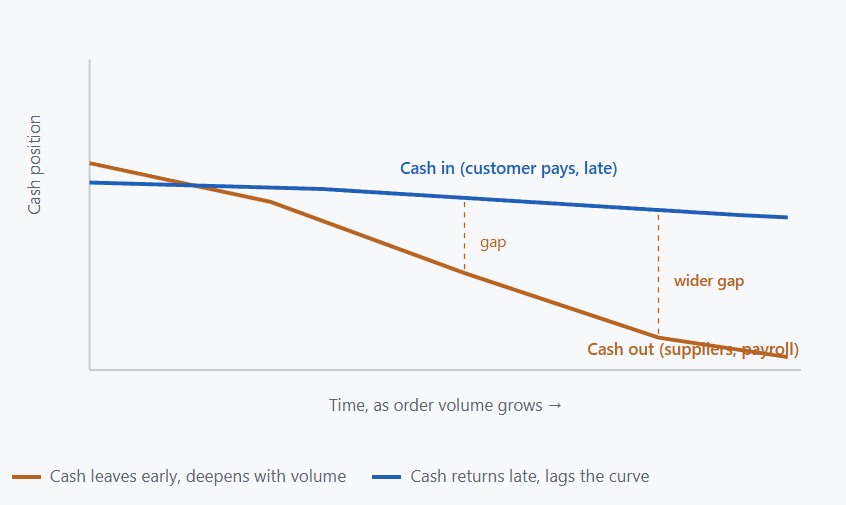

Visual 2 — The cash gap widens with volume

Conceptual model. Money goes out the door for suppliers and payroll well before customers pay. As volume rises, the cash-out curve falls faster than the cash-in curve catches up — and the distance between them is the capital you must finance just to stay open.

The levers nobody pulls

What makes this maddening is that the cash gap is highly controllable, and the controls sit in plain sight. They just live in places leaders rarely look because none of them move the profit line.

Supplier terms are a negotiation, not a given — moving from net-30 to net-60 on the payables side keeps your cash longer at no cost to margin. Collections is treated as a clerical afterthought when it is, in real terms, the difference between solvency and a bridge loan; a week shaved off your average collection period frees real money. Inventory is cash wearing a costume, sitting on a shelf doing nothing until it sells. And billing cadence — whether you invoice on milestones or wait until the end, whether you ask for deposits, whether you bill the day the work ships or three weeks later out of politeness — quietly sets how deep your hole runs. None of these appear on the P&L. All of them decide whether you survive.

Why 2026 makes the gap costlier

For a decade, a wide cash gap was an annoyance you could paper over cheaply. Money was nearly free; you funded the hole with a credit line at a rate that barely registered. That subsidy is gone. With the cost of capital sitting at a structurally higher plateau, every day a dollar spends trapped in the cash cycle now carries a real, compounding price. The same 70-day gap that cost a rounding error in 2021 is an expensive habit in 2026.

The companies feeling this most acutely are exactly the ones that look healthiest on paper — the fast growers funding their working capital on borrowed money at rates that finally bite. Profitable, expanding, and quietly bleeding from a wound the income statement was never designed to show.

What this means for leaders

Put cash on the same slide as profit, every time. If your board deck leads with revenue and net income and buries the cash conversion cycle in an appendix, you are managing the opinion and ignoring the fact. The single most useful number for most growing companies isn't margin — it's how many days of cash the business has and which direction that number is moving.

Treat the cash cycle as an operating discipline, not an accounting chore. Terms, collections, inventory, and billing cadence are leadership decisions with survival-level consequences. Hand them to a clerk and you've handed away the thing that determines whether the company makes it. A focused effort to shrink the gap by twenty days can be worth more than a quarter of margin improvement.

Respect growth as the cash hazard it is. When you plan to grow 50 percent next year, ask the second question nobody asks: what will it cost to fund that growth before the cash comes back? If you can't answer it, you don't have a growth plan. You have a hope, financed by a hole.

Companies rarely die because the business model failed. They die because the money ran out while the model was still working. Profit tells you the story is good. Cash tells you whether you live to finish it.

A LookatBusiness original framework. The cash conversion cycle bites harder in 2026: with the cost of capital sitting at a structurally higher plateau than the last decade, every day a dollar spends trapped between paying suppliers and collecting from customers carries a real, compounding financing cost — making a wide cash gap meaningfully more expensive to carry than it was three years ago.